「Vintage Stablecoin」 Depegs Overnight, Evaporating $18 Million - Can Synthetix's sUSD Still Buy the Dip?

This unplanned depegging occurred as a temporary "side effect" of Synthetix's upgrade to the "420 Pool" mechanism.

The crypto world is ever-changing, and the word "stable" in stablecoins often faces many tests. On April 10, the stablecoin sUSD in the Synthetix ecosystem experienced a significant deviation from its peg, with the lowest price dropping to $0.834. It is currently trading at $0.860, deviating by approximately 14% from its $1 anchor value. This rapid fluctuation quickly sparked community discussions, with many worried that this could be a signal of a new stablecoin crisis.

Mechanism Upgrade Leads to Short-Term Deviation

After the event, Synthetix founder Kain Warwick explained the situation on the X platform and revealed that he had sold 90% of his ETH holdings and increased his SNX position. Warwick stated that the sUSD deviation was not a sign of a systemic crisis but a temporary "side effect" caused by a critical mechanism upgrade in Synthetix.

This should be the second deviation event in sUSD's history. The last one was on May 17, 2024, but the reasons were different. According to the blockchain security firm Chaos Labs, last year's deviation was likely caused by a major sBTC/wBTC liquidity provider suddenly withdrawing funds, redeeming sUSD through Synthetix's spot synthetic redemption mechanism, and then selling a large amount in the related Curve liquidity pool.

For a long time, sUSD's stability relied on a complex debt management mechanism: users collateralized the native token SNX to mint sUSD, and the system maintained its 1:1 peg to the dollar through high collateralization and debt adjustment. With the adjustment of Synthetix's strategic direction, this old mechanism has gradually been removed, replaced by a more efficient, decentralized new system—the "420 Pool" under the SIP-420 proposal. The transition between the old and new mechanisms inevitably brought about growing pains, and the short-term deviation of sUSD is a manifestation of this process.

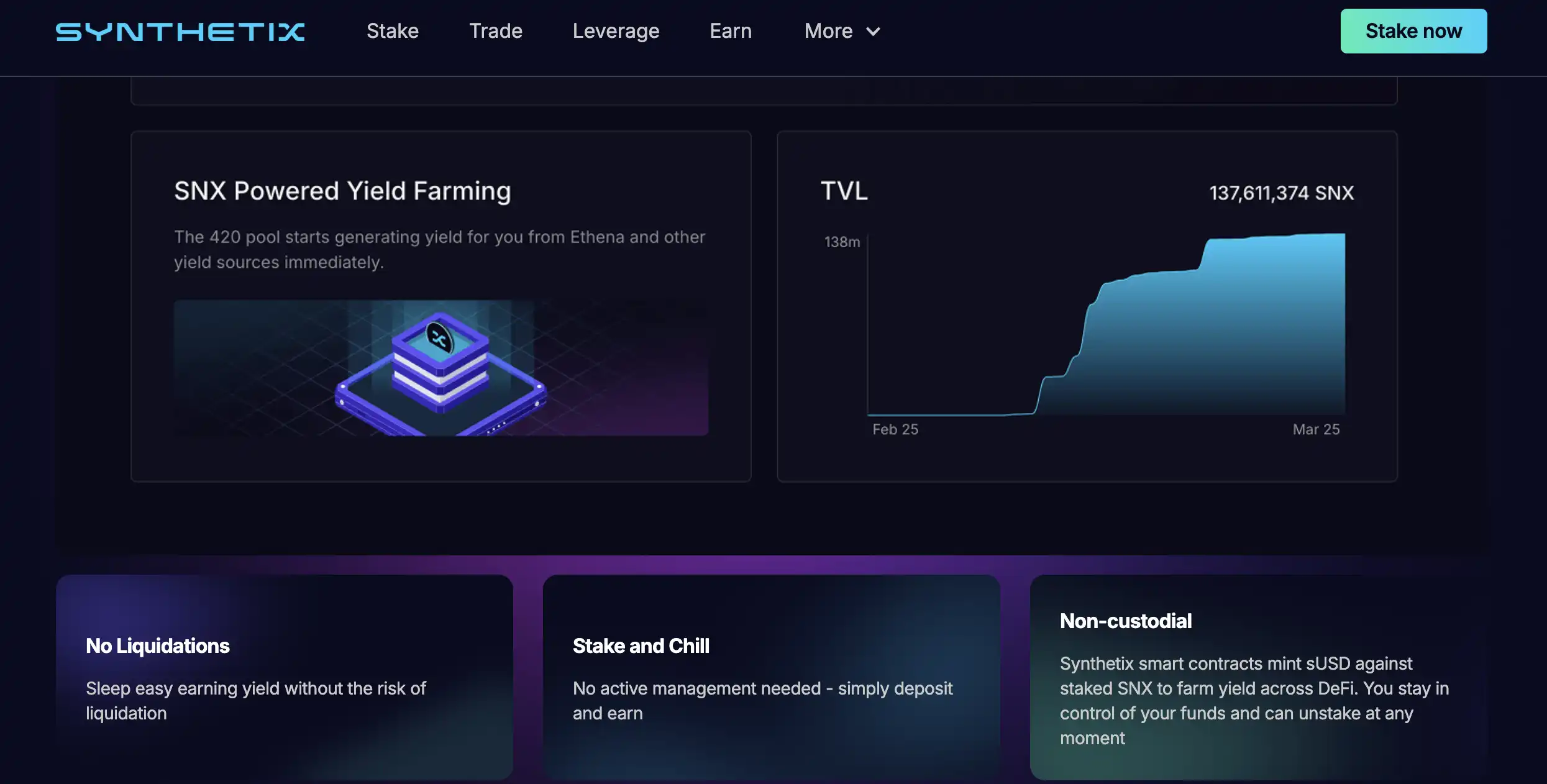

The 420 Pool introduced by the SIP-420 proposal allows SNX holders to deposit tokens into a collectively managed pool. This pool's design has brought several key changes. Firstly, pledgers no longer need to bear high debt and liquidation risks individually. Under the old mechanism, individuals had to maintain a 500% collateralization ratio when minting sUSD by pledging SNX, meaning that for every $5 worth of SNX pledged, only $1 of sUSD could be minted. In the new mechanism, the 420 Pool has reduced the collateralization ratio to 200%, allowing $2 worth of SNX to mint $1 of sUSD, increasing minting capacity by 2.5 times. This change has attracted the participation of a large number of SNX holders—during the whitelist period, over 80 million SNX were deposited into the pool.

However, this increased minting capacity directly led to a surge in the sUSD supply. Based on a 200% collateralization ratio, assuming that the deposited 80 million SNX were worth around $160 million (estimated at $2 per SNX), theoretically, sUSD worth $80 million could be minted. Prior to this, the same amount of SNX could only mint around $32 million worth of sUSD. The sudden supply increase, without a corresponding matching market demand, inevitably put downward pressure on the sUSD price. More specifically, many stakers minted sUSD and used it for yield farming activities, such as participating in external strategies like Ethena Labs, Aave, or MorphoLabs. These actions often involved selling sUSD on secondary markets to acquire other assets, further exacerbating the selling pressure.

At the same time, the peg mechanism of sUSD also became less effective due to the implementation of SIP-420. Under the old mechanism, when the sUSD price fell below $1, there was a direct arbitrage opportunity: users could buy sUSD at a lower price and then use it to repay debt or exchange for other synthetic assets (such as sBTC), profiting from it and driving the price back up to $1. This arbitrage behavior was a key force in maintaining the sUSD peg. However, the 420 pool change altered this dynamic. Under the new mechanism, individual debts are gradually shifted to protocol management and forgiven over a 12-month period, so stakers no longer need to frequently adjust their debt positions to avoid liquidation. While this eliminated liquidation risk, it also weakened the direct arbitrage incentive and capability. As debt management is more taken over by the SNX Exchange, there is insufficient market force to swiftly correct sUSD price deviations through traditional means.

Therefore, the core reasons for sUSD's deviation from its peg can be attributed to two factors: first, the supply increased significantly due to the lower collateralization ratio, and second, the old peg maintenance mechanism became ineffective during the transition period, causing the market to be unable to efficiently absorb the excess sUSD. Nevertheless, the collateralized nature of sUSD ensures that it is not entirely unsupported. A 200% collateralization ratio means that behind every $1 of sUSD, there are still $2 of SNX as collateral, which is fundamentally different from algorithmic stablecoins like Terra's UST that rely on uncollateralized supply-demand adjustments. Even if the price temporarily deviates from $1, the over-collateralization feature of sUSD prevents it from facing systemic collapse risks.

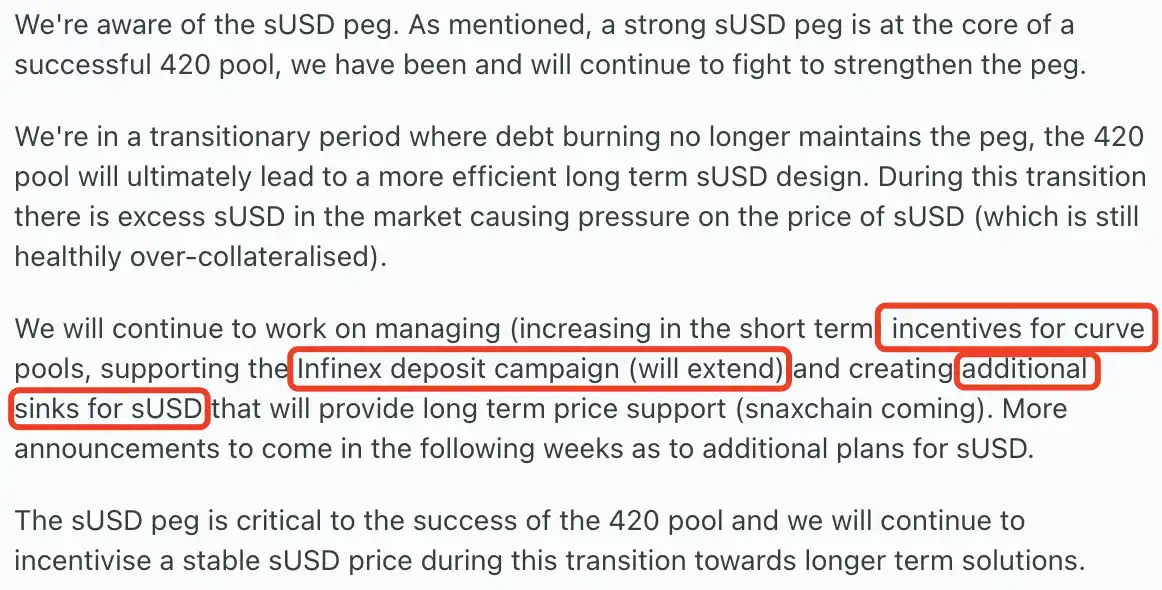

For SNX holders and sUSD users, the team has devised a transitional plan. The Synthetix team further elaborated on the mitigation measures through Discord, including strengthening incentives for the Curve pool in the short term, extending support for the Infinex deposit event, and building a long-term price support system for sUSD.

Attention Drawn to "Antique Stablecoin" Depegging, What Has Synthetix Been Up To Lately?

To further understand the current situation of sUSD, let's first review the development history of stablecoins. The origin of stablecoins can be traced back to 2014, a year that witnessed the birth of the first stablecoins: Tether's USDT, BitShares' bitUSD, and Nubits. Although bitUSD and Nubits did not stand the test of time and gradually faded into obscurity, USDT has survived to this day with its first-mover advantage and strong market adaptability, becoming the world's largest stablecoin by trading volume. The success of USDT has not been without challenges, as its price experienced significant decoupling in 2017. However, to this day, USDT still firmly holds the position of the leading stablecoin.

2018 was another key milestone in stablecoin development. That year, DeFi began to rise, leading to the emergence of several iconic stablecoins. MakerDAO's DAI, Synthetix's sUSD, and Terra's UST made their debut. Meanwhile, the CeFi sector also witnessed a second wave of stablecoin fever, including Circle's USDC, TrueUSD (TUSD), Gemini's GUSD, and Paxos' PAX. These projects each had their own characteristics: DAI achieved decentralized stability through overcollateralizing ETH, sUSD supported a synthetic asset ecosystem with a high collateralization rate of SNX, and USDC differentiated itself with its redeemable fiat reserves. Throughout this history, different types of stablecoins gradually diverged into two main paths: collateralized and algorithmic. Collateralized stablecoins are backed by real-world assets, providing relatively high stability but are susceptible to collateral price fluctuations. On the other hand, algorithmic stablecoins maintain their peg through smart contract-driven supply-demand adjustments, theoretically achieving higher capital efficiency but risk losing control during market volatility.

In 2021, DeFi projects widely recognized the strategic value of having their own stablecoins, prompting many protocols to heavily develop their stablecoin ecosystems. However, Synthetix chose to gradually sideline sUSD, a move that is undoubtedly viewed as a significant mistake in hindsight. The SIP 420 proposal passed in early 2025 brought new opportunities for sUSD. The new mechanism introduced a pooled collateral model, reduced the collateralization ratio to 200%, and planned to forgive $62 million in historical debt over 12 months, significantly improving capital efficiency and system security. While the old debt destruction mechanism became ineffective and the new stability module was not yet fully in place, this depegging incident was a result of the transition period.

Looking around, the competition in the stablecoin space remains fierce. Although sUSD is still the third "longest-lived" stablecoin in the cryptocurrency space, although its status is not as prominent as before, its survival time (i.e., Lindy effect) has given it a unique resilience. The recent protocol adjustments may just be another upgrade on its evolutionary path.

In the short term, the price of sUSD may continue to fluctuate in a 5-10% discount range, but with a sufficient reserve in the treasury, the possibility of a complete collapse is low. In the long run, with the implementation of the new mechanism, sUSD is expected to regain its foothold in the Synthetix ecosystem. The history of stablecoins tells us that the real strong ones are often survivors who continuously adjust in the storms.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

RFCUSDT now launched for futures trading and trading bots

Bitget Spot Bot adds RFC/USDT

Checkmate: How Adopting a BRICS Payment System Might Erode the Dollar’s Dominance in Trade Markets

Fake McAfee pop-ups fuel Bitcoin and gold scams