sUSD Depreciates by 16%: Stablecoin Myth Busted or Buying Opportunity?

This issue stems from the mechanism adjustment transitional period triggered by SIP-420 proposal, resulting in a temporary loss of sUSD's peg stabilization ability.

Original Title: "sUSD Depegging by 16%: A Shattered Stablecoin Myth or a Buy-the-Dip Opportunity?"

Original Author: Oliver, Mars Finance

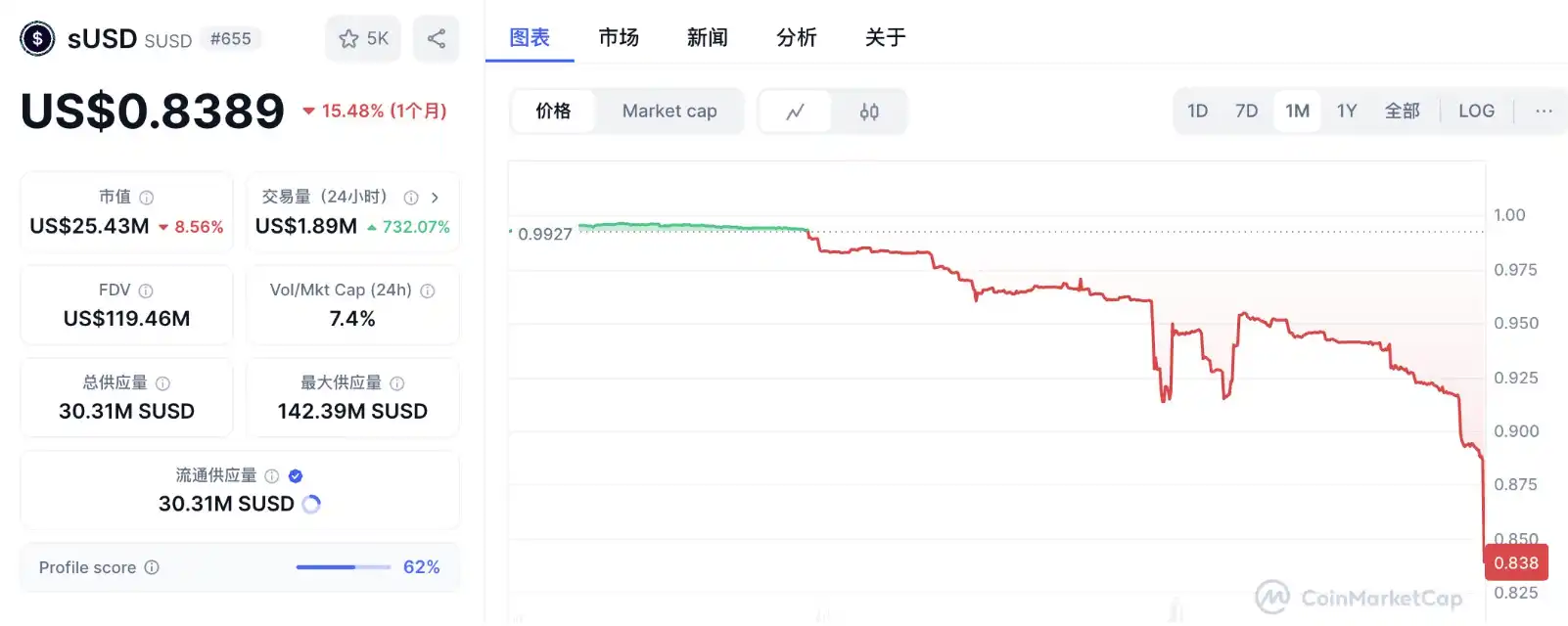

The core stablecoin of the Synthetix ecosystem, sUSD, has recently been deeply embroiled in a depegging quagmire. As of April 9, 2025, its price fell to around $0.8388, deviating over 16% from its theoretical $1 peg, attracting significant market attention. This crisis began on March 20 and has lasted for over 20 days, with the depegging magnitude continuing to expand. Meanwhile, the native token of Synthetix, SNX, has been rising against the trend, with a daily increase of 7.5%, displaying a complex market sentiment. Kain Warwick, the founder of Synthetix (@kaiynne), attributed the depegging to the transitional pains of mechanism adjustments and revealed that the protocol has sold 90% of its ETH position and increased its SNX holdings to cope.

Timeline of Events: The Progressive Deterioration of Depegging

The depegging of sUSD did not occur overnight. On March 20, 2025, its price first showed a slight deviation, initially not raising widespread alarm. However, as time passed, the volatility gradually evolved into a downward trend. By April 9, according to CoinMarketCap data, the quoted sUSD price had dropped to $0.8388, more than 16% below the pegged value. This depegging, lasting for over 20 days, not only exceeded the expected timeframe but also far surpassed the market's typical tolerance range for stablecoins, revealing the deep-seated complexity of the issue.

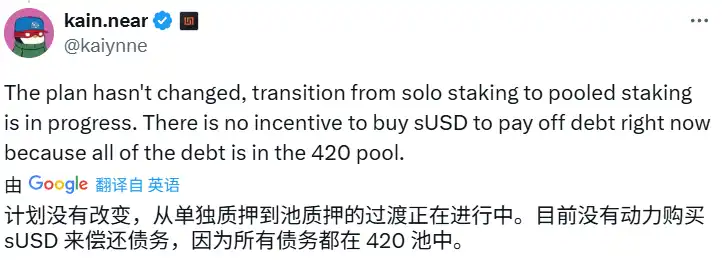

Kain Warwick explained this on the X platform, stating that the depegging was an expected side effect of the SIP-420 proposal's implementation. The proposal aimed to optimize the SNX staking mechanism and capital efficiency by introducing a centralized debt pool (the "420 Pool"); however, the alternation between old and new mechanisms temporarily disrupted sUSD's peg repairability. He frankly stated that at this stage, there is "no incentive for users to buy sUSD to repay debt," and the imbalance of supply and demand became the direct driver of the price decline. Additionally, the protocol's strategy of selling 90% of its ETH position and increasing its SNX holdings, while intended to strengthen internal support, may have weakened the system's liquidity and external stability foundation, adding more uncertainty to the market.

Depegging Root Cause: The Overlay of Mechanism Transition and Market Feedback

The root cause of this recent de-pegging was not singular but rather a result of intertwined mechanism adjustments and market behaviors, presenting a multi-dimensional challenge.

The implementation of SIP-420 was the core trigger of the crisis. Synthetix's stablecoin mechanism relies on overcollateralization of SNX, where users stake SNX to mint sUSD and bear the fluctuation risk of the system's debt pool. Under the old mechanism, a collateralization ratio of up to 750% and debt repayment incentives collectively maintained the stability of sUSD. However, SIP-420 shifted the individual staking model to a centralized debt pool, aiming to enhance the attractiveness of SNX staking. This transition theoretically injected long-term potential into the ecosystem, but during the transition period, it disrupted the existing equilibrium. Warwick admitted that the new mechanism has not yet fully matured, and the old anchoring stabilization feature was temporarily suspended, causing sUSD to lose its self-regulating mechanism.

Market behaviors further amplified the de-pegging effect. Data from X platform indicated that some users concentratedly exchanged sUSD for USDT or USDC on decentralized trading platforms like Curve, depleting the liquidity pool's balance through selling pressure rapidly. Taking the Curve DAI-USDC-USDT-sUSD pool as an example, the proportion of sUSD temporarily surged, reflecting a decline in market confidence in stability. With a market cap of only $25 million, sUSD itself had weak liquidity, and any concentrated selling could trigger significant slippage, causing the price to further deviate from its peg.

Protocol-level adjustments also brought about unexpected side effects. The decision to sell 90% of ETH and increase SNX holdings, while strengthening SNX's dominant position in the ecosystem, reduced the system's diversification support. ETH, as a widely accepted collateral in the market, exiting could diminish external trust in sUSD, while SNX's volatility increased concentration risk. This strategy might boost confidence during an SNX price increase, but amid a prolonged de-pegging scenario, it instead cast a shadow over the recovery process.

Historical Comparison

This is not the first time sUSD has de-pegged. Looking back to May 16, 2024, sUSD fell to $0.915 due to a whale selling sBTC for sUSD, causing a de-pegging of approximately 8.5%. At that time, insufficient Curve pool liquidity combined with MEV arbitrage bots' sniper attacks led to a brief price loss of control. Synthetix promptly took action by adding collateral such as ETH, BTC, USDC to boost confidence and providing liquidity incentives on Velodrome and Curve, successfully re-anchoring to $1 after 11 days. That de-pegging event was essentially an external shock, with the mechanism itself remaining intact and a clear and efficient path to recovery.

In contrast, the 2025 anchor break presents a starkly different scenario. This crisis stemmed from internal mechanism adjustments under SIP-420, rather than a singular external sell-off, significantly increasing the complexity of the issue. The 2024 anchor break lasted for 11 days with an 8.5% drop, while the current one has surpassed 20 days with a drop of over 16%, indicating the severity and persistence of the problem. Furthermore, the response in 2024 relied on liquidity incentives and collateral diversification, whereas the 2025 strategy leans more towards internal adjustments (such as selling ETH to increase SNX exposure), with short-term effects yet to materialize. This indicates that the experiences of 2024 cannot be directly applied, with the repair difficulty far exceeding the past.

Feasibility Analysis of Buying the Dip in sUSD

The current sUSD price hovers around $0.84. For investors, is it feasible to buy the dip and wait for a re-anchor? The experience of 2024 provides some insights. Back then, sUSD rebounded from $0.915 to $1, and dip buyers saw around a 9% return within two weeks, with the key to success lying in quick incentive measures and the short-lived nature of external shocks. Now the price is lower ($0.84), the potential returns are higher (around 19%), but the risks are also magnified.

Positive factors should not be overlooked. The 7.5% increase in SNX reflects market confidence in Synthetix remaining intact, with the team's proactive stance and debt relief plan injecting hope into the recovery. With a small market cap, sUSD requires low funds, and if the protocol introduces incentives, even small buy orders can drive up the price. However, the risks are significant as well. The anchor break has exceeded 20 days, and the duration is unknown. If new mechanism debugging is delayed, the repair may be prolonged for months. Selling pressure remains, pool imbalances on Curve may further depress prices, and the loss of user confidence may weaken demand.

Using $100,000 as an example, buying around 119,000 sUSD at $0.84, if it re-anchors to $1, one could profit $19,000, with a return of 19%. However, it is advised to set a stop-loss level (e.g., $0.75) and closely monitor protocol announcements. If Synthetix introduces incentives similar to those in 2024, the odds of buying the dip will significantly increase. If the price stabilizes and SNX continues to rise, a small position can be established. Compared to the low-risk window of 2024, this opportunity offers higher returns but comes with greater uncertainty.

Market Response and SNX's Anomaly

Despite sUSD being deeply embroiled in an anchor break crisis, SNX recorded a 7.5% single-day increase on April 9th, a striking contrast. The market's optimism may stem from expectations of long-term benefits from SIP-420. If the new mechanism is successfully implemented, it could enhance SNX's staking rewards and ecosystem position, boosting Synthetix's competitiveness in the DeFi space. The "Debt Jubilee" debt relief plan mentioned by Warwick may also inject confidence into investors, implying that clearing historical debts will lighten the system's burden.

The community reaction has been polarized. On the X platform, some users are concerned that sUSD may fall into a "death spiral," questioning the rationale behind the mechanism adjustment. On the other hand, some believe that the $25 million market cap of sUSD has limited impact, and that SNX's rise is the true reflection of market confidence. Professional analysis firms such as The Merkle News have pointed out that the transitional risk of SIP-420 was underestimated, but SNX's performance indicates that Synthetix still has the potential to turn the situation around.

Summary

From an industry perspective, the impact of sUSD's de-pegging is relatively limited. Its $25 million market cap is negligible in the stablecoin market, far below the scale of USDT or USDC, and has a small spillover effect on the DeFi ecosystem. However, for Synthetix internally, persistent de-pegging may shake user trust. If liquidity continues to drain from the pools, the utility of sUSD will be limited, further weakening its position in synthetic asset trading.

In the short term, intensified de-pegging may lead to more sell-offs, putting further pressure on the price. However, SNX's resilience has bought the protocol a time window. If the new mechanism can stabilize in the coming weeks, coupled with a debt relief plan, sUSD still has a chance to re-peg. In the long term, Synthetix needs to learn from this crisis, optimize stablecoin design, and avoid a similar crisis recurrence. The success of the mechanism adjustment will determine whether it can stand firm in the fiercely competitive DeFi market.

Unlike the external shock of 2024, the endogeneity of this crisis makes its path to recovery more tortuous. The Synthetix team must work on both mechanism optimization and rebuilding market confidence to weather the storm. For investors, the $0.84 sUSD is both a risk exposure and a potential opportunity. Whether bottom fishing or waiting and watching, closely monitoring the protocol's subsequent dynamics will be crucial. In this de-pegging storm, Synthetix's future direction is worth continuous tracking.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

RFCUSDT now launched for futures trading and trading bots

Bitget Spot Bot adds RFC/USDT

Checkmate: How Adopting a BRICS Payment System Might Erode the Dollar’s Dominance in Trade Markets

Fake McAfee pop-ups fuel Bitcoin and gold scams